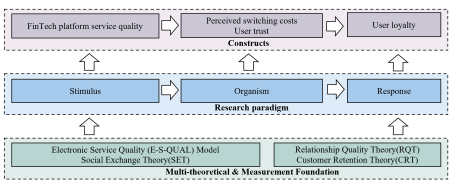

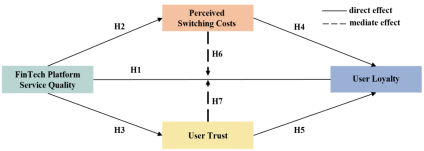

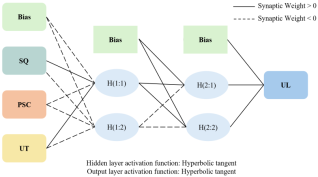

This study examines how FinTech platform service quality influences user loyalty in China, and focuses on two mediators: perceived switching costs and user trust. Data were collected from 290 Chinese commercial bank customers with active FinTech platform usage experience, using purposive sampling to ensure respondents had sufficient experience to evaluate the services. A hybrid Structural Equation Modeling-Artificial Neural Network (SEM-ANN) Approach is applied to test both linear and non-linear relationships. The findings from SEM show that service quality has positive effects on perceived switching costs, user trust, and user loyalty. User trust also positively affects loyalty. However, perceived switching costs do not show a significant direct effect on loyalty. This suggests that in mature markets, trust matters more than switching barriers. For mediation, user trust plays a significant partial mediating role. The indirect path through perceived switching costs is not significant. ANN sensitivity analysis confirms this: user trust has the highest predictive importance (100%), followed by service quality (78.29%). Perceived switching costs rank lowest (31.35%). This study makes contributions by verifying the dual-mediator model in China’s mature FinTech context, providing a framework for customer retention. Bank managers should build trust via service quality instead of artificial switching barriers.

| Published in | International Journal of Economics, Finance and Management Sciences (Volume 14, Issue 3) |

| DOI | 10.11648/j.ijefm.20261403.14 |

| Page(s) | 225-234 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

FinTech Platform Service Quality, Perceived Switching Costs, User Trust, User Loyalty, PLS-SEM-ANN

Demographic | Categories | Frequency | Percent |

|---|---|---|---|

Gender | Male | 130 | 44.828% |

Female | 160 | 55.172% | |

Age groups | < 18 | 45 | 15.517% |

18–30 | 106 | 36.551% | |

31–40 | 107 | 36.897% | |

41–50 | 23 | 7.931% | |

51–60 | 3 | 1.034% | |

> 60 | 6 | 2.069% | |

Education | Junior high school or below | 29 | 10.000% |

High secondary school | 62 | 21.379% | |

College | 73 | 25.172% | |

Undergraduate | 100 | 34.483% | |

Postgraduate or above | 26 | 8.966% | |

Profession | Student | 48 | 16.558% |

Enterprise employee | 171 | 59.966% | |

Government institution staff | 44 | 15.172% | |

Freelancer | 27 | 9.310% | |

Using time of FinTech platform | 1–3 years | 99 | 34.138% |

More than 3 years | 191 | 65.862% |

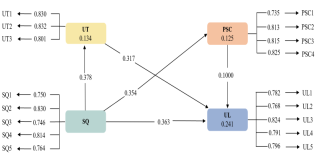

Constructs | α | CR | AVE |

|---|---|---|---|

SQ | 0.888 | 0.888 | 0.614 |

PSC | 0.875 | 0.875 | 0.637 |

UT | 0.861 | 0.861 | 0.674 |

UL | 0.894 | 0.894 | 0.628 |

Fornell-Larcker Criterion | ||||

SQ | PSC | UT | UL | |

SQ | 0.784 | |||

PSC | 0.354 | 0.798 | ||

UT | 0.378 | 0.356 | 0.821 | |

UL | 0.363 | 0.287 | 0.432 | 0.793 |

HTMT Criterion | ||||

SQ | PSC | UT | UL | |

SQ | ||||

PSC | 0.402 | |||

UT | 0.459 | 0.444 | ||

UL | 0.406 | 0.338 | 0.525 | |

Hypotheses | SD |

| t-value | p-value | Result | 95%CI |

|---|---|---|---|---|---|---|

Direct Effects | ||||||

H1: SQ →UL | 0.066 | 0.363 | 6.518 | < 0.001 | Supported | [0.242,0.461] |

H2: SQ →PSC | 0.054 | 0.354 | 6.619 | < 0.001 | Supported | [0.235,0.446] |

H3: SQ →UT | 0.054 | 0.378 | 7.010 | < 0.001 | Supported | [0.263,0.475] |

H4: PSC →UL | 0.060 | 0.100 | 1.674 | 0.094 | Rejected | [-0.017,0.219] |

H5: UT →UL | 0.063 | 0.317 | 5.047 | < 0.001 | Supported | [0.190,0.437] |

Mediation Effects | ||||||

H6: SQ →PSC →UL | 0.023 | 0.036 | 1.573 | 0.116 | Rejected | [-0.006,0.085] |

H7: SQ →UT →UL | 0.030 | 0.120 | 4.019 | < 0.001 | Supported | [0.067,0.183] |

Neural networks | RMSE (Training) | RMSE (Testing) | Total Sample | SQ | PSC | UT |

|---|---|---|---|---|---|---|

ANN1 | 0.758 | 0.831 | 290 | 0.337 | 0.156 | 0.507 |

ANN2 | 0.767 | 0.825 | 290 | 0.257 | 0.169 | 0.574 |

ANN3 | 0.770 | 0.784 | 290 | 0.303 | 0.127 | 0.570 |

ANN4 | 0.745 | 0.821 | 290 | 0.378 | 0.177 | 0.445 |

ANN5 | 0.871 | 0.664 | 290 | 0.400 | 0.139 | 0.462 |

ANN6 | 0.794 | 0.898 | 290 | 0.526 | 0.018 | 0.457 |

ANN7 | 0.795 | 0.738 | 290 | 0.376 | 0.176 | 0.449 |

ANN8 | 0.786 | 0.769 | 290 | 0.455 | 0.211 | 0.334 |

ANN9 | 0.815 | 0.679 | 290 | 0.369 | 0.137 | 0.496 |

ANN10 | 0.763 | 0.778 | 290 | 0.335 | 0.186 | 0.479 |

Mean | 0.786 | 0.778 | 0.374 | 0.149 | 0.477 | |

SD | 0.036 | 0.071 | ||||

NI | 78.290 | 31.349 | 100 |

ANN | Artificial Neural Network |

AVE | Average Variance Extracted |

CMV | Common Method Variance |

CR | Composite Reliability |

CRT | Customer Retention Theory |

E-S-QUAL | Electronic Service Quality |

f² | Effect Size |

HTMT | Heterotrait-Monotrait Ratio |

MLP | Multilayer Perceptron |

NI | Normalized Importance |

PSC | Perceived Switching Costs |

PLS-SEM | Partial Least Squares Structural Equation Modeling |

R² | Coefficient of Determination |

RMSE | Root Mean Square Error |

RQT | Relationship Quality Theory |

SD | Standard Deviation |

SEM | Structural Equation Modeling |

SET | Social Exchange Theory |

S-O-R | Stimulus-Organism-Response |

SQ | Service Quality |

UL | User Loyalty |

UT | User Trust |

VIF | Variance Inflation Factor |

| [1] | Kim, L., Jindabot, T., Yeo, S. F. (2024). Understanding customer loyalty in banking industry: A systematic review and meta analysis. Heliyon, 10(17), e36619. |

| [2] | Chauhan, S., Akhtar, A., & Gupta, A. (2022). Customer experience in digital banking: A review and future research directions. International Journal of Quality and Service Sciences, 14(2), 311-348. |

| [3] | Sharma, N., & Singh, B. (2024). Exploring the impact of financial inclusion on socio-demographic factors with digital banking adoption. XIBA Business Review, 7(2), 05-17. |

| [4] | Mackay, A. C., Zuo, L., & Kebe, I. A. (2025). Driving customer loyalty in digital banking: The mediating role of engagement and the moderating role of switching costs. South African Journal of Business Management, 56(1), 5112. |

| [5] | Sharma, V., Jangir, K., Gupta, M., & Rupeika-Apoga, R. (2024). Does service quality matter in FinTech payment services? An integrated SERVQUAL and TAM approach. International Journal of Information Management Data Insights, 4(2), 100252. |

| [6] | Hennig-Thurau, T., Gwinner, K. P., & Gremler, D. D. (2002). Understanding relationship marketing outcomes: An integration of relational benefits and relationship quality. Journal of Service Research, 4(3), 230-247. |

| [7] | Mehrabian, A., & Russell, J. A. (1974). An Approach to Environmental Psychology. The MIT Press. |

| [8] | Blau, P. M. (1964). Exchange and Power in Social Life. John Wiley & Sons. |

| [9] | Cropanzano, R., & Mitchell, M. S. (2005). Social exchange theory: An interdisciplinary review. Journal of Management, 31(6), 874-900. |

| [10] | Abbas, M. A. (2025). Customer satisfaction as a mediator between FinTech service quality and loyalty: An SEM-based analysis. Lead Sci Journal of Management, Innovation and Social Sciences, 1(3), 42-53. |

| [11] | Parasuraman, A., Zeithaml, V. A., & Malhotra, A. (2005). E-S-QUAL: A multiple-item scale for assessing electronic service quality. Journal of Service Research, 7(3), 213-233. |

| [12] | Homans, G. C. (1958). Social behavior as exchange. American Journal of Sociology, 63(6), 597-606. |

| [13] | Tuong, V. D., Thach, N. H., Khanh, P. N. K., Han, L. T. B., & Thanh, P. T. K. (2025). Understanding gen Z’s digital banking loyalty: The role of switching costs and consumption values. Journal of Organizational Behavior Research, 10(1), 44-57. |

| [14] | Nguyen, D. T., Pham, V. T., Tran, D. M., & Pham, D. B. T. (2020). Impact of service quality, customer satisfaction and switching costs on customer loyalty. The Journal of Asian Finance, Economics and Business, 7(8), 395-405. |

| [15] | Mayer, R. C., Davis, J. H., & Schoorman, F. D. (1995). An integrative model of organizational trust. Academy of Management Review, 20(3), 709-734. |

| [16] | Khan, I., Hollebeek, L., Fatma, M., Islam, J., Rather, R. A., Shahid, S., & Sigurdsson, V. (2023). Mobile app vs. desktop browser platforms: the relationships among customer engagement, experience, relationship quality and loyalty intention. Journal of Marketing Management, 39(3-4), 275-297. |

| [17] | Luo, X., Li, H., Zhang, J., & Shim, J. P. (2010). Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems, 49(2), 222-234. |

| [18] | Alnaim, A. F., Sobaih, A. E. E., & Elshaer, I. A. (2022). Measuring the mediating roles of e-trust and e-satisfaction in the relationship between e-service quality and e-loyalty: A structural modeling approach. Mathematics, 10(13), 2328. |

| [19] | Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2-24. |

| [20] | Albahri, A. S., Alnoor, A., Zaidan, A. A., Albahri, O. S., Hameed, H., Zaidan, B. B., Peh, S. S., Zain, A. B., Siraj, S. B., Masnan, A. H. B., & Yass, A. A. (2022). Hybrid artificial neural network and structural equation modelling techniques: a survey. Complex and Intelligent Systems, 8(2), 1781-1801. |

| [21] | Jose, A., Mathew, S., G, R., Chacko, D. P., & Thomas, A. K. (2022). The role of switching cost in the e-service recovery framework among banking customers. International Journal of Quality and Service Sciences, 14(1), 86-109. |

| [22] | Martínez-Navalón, J. G., Fernández-Fernández, M., & Alberto, F. P. (2023). Does privacy and ease of use influence user trust in digital banking applications in Spain and Portugal?. International Entrepreneurship and Management Journal, 19(2), 781-803. |

| [23] | Arora, P., & Banerji, R. (2024). The impact of digital banking service quality on customer loyalty: An interplay between customer experience and customer satisfaction. Asian Economic and Financial Review, 14(9), 712-733. |

| [24] | Thach, N. H., Bui, H. K., Thanh, P. T. K., Thuong, C. T., & Ghi, T. N. (2025). Exploring Customer Loyalty in Vietnam’s Digital Banking Industry: Insights from switching costs and alternative attractiveness. International Review of Management and Marketing, 15(4), 269-280. |

| [25] | Kock, N., & Hadaya, P. (2018). Minimum sample size estimation in PLS‐SEM: The inverse square root and gamma‐exponential methods. Information Systems Journal, 28(1), 227-261. |

| [26] | Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of e-Collaboration (ijec), 11(4), 1-10. |

| [27] | Kock, N., & Lynn, G. S. (2012). Lateral collinearity and misleading results in variance-based SEM: An illustration and recommendations. Journal of the Association for Information Systems, 13(7), 546-580. |

| [28] | Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50. |

| [29] | Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43, 115-135. |

| [30] | Judijanto, L., Ariyanti, R., & Suryani, S. (2024). Analysis of the impact of mobile banking technology, fintech, and digital transaction security on customer loyalty at BUMN Banks in Indonesia. West Science Social and Humanities Studies, 2(08), 1299-1309. |

| [31] | Changalima, I. A., & Chuwa, M. P. (2025). Partial least squares structural equation modeling (PLS-SEM) in business research: A simple guide for novice researchers. International Journal of Research in Business and Social Science (2147-4478), 14(9), 497-506. |

APA Style

Wang, Y., Li, T. (2026). Linking FinTech Platform Service Quality and User Loyalty: The Mediating Roles of Perceived Switching Costs and User Trust via a SEM-ANN Approach. International Journal of Economics, Finance and Management Sciences, 14(3), 225-234. https://doi.org/10.11648/j.ijefm.20261403.14

ACS Style

Wang, Y.; Li, T. Linking FinTech Platform Service Quality and User Loyalty: The Mediating Roles of Perceived Switching Costs and User Trust via a SEM-ANN Approach. Int. J. Econ. Finance Manag. Sci. 2026, 14(3), 225-234. doi: 10.11648/j.ijefm.20261403.14

@article{10.11648/j.ijefm.20261403.14,

author = {Yuxin Wang and Tengyu Li},

title = {Linking FinTech Platform Service Quality and User Loyalty: The Mediating Roles of Perceived Switching Costs and User Trust via a SEM-ANN Approach},

journal = {International Journal of Economics, Finance and Management Sciences},

volume = {14},

number = {3},

pages = {225-234},

doi = {10.11648/j.ijefm.20261403.14},

url = {https://doi.org/10.11648/j.ijefm.20261403.14},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijefm.20261403.14},

abstract = {This study examines how FinTech platform service quality influences user loyalty in China, and focuses on two mediators: perceived switching costs and user trust. Data were collected from 290 Chinese commercial bank customers with active FinTech platform usage experience, using purposive sampling to ensure respondents had sufficient experience to evaluate the services. A hybrid Structural Equation Modeling-Artificial Neural Network (SEM-ANN) Approach is applied to test both linear and non-linear relationships. The findings from SEM show that service quality has positive effects on perceived switching costs, user trust, and user loyalty. User trust also positively affects loyalty. However, perceived switching costs do not show a significant direct effect on loyalty. This suggests that in mature markets, trust matters more than switching barriers. For mediation, user trust plays a significant partial mediating role. The indirect path through perceived switching costs is not significant. ANN sensitivity analysis confirms this: user trust has the highest predictive importance (100%), followed by service quality (78.29%). Perceived switching costs rank lowest (31.35%). This study makes contributions by verifying the dual-mediator model in China’s mature FinTech context, providing a framework for customer retention. Bank managers should build trust via service quality instead of artificial switching barriers.},

year = {2026}

}

TY - JOUR T1 - Linking FinTech Platform Service Quality and User Loyalty: The Mediating Roles of Perceived Switching Costs and User Trust via a SEM-ANN Approach AU - Yuxin Wang AU - Tengyu Li Y1 - 2026/06/09 PY - 2026 N1 - https://doi.org/10.11648/j.ijefm.20261403.14 DO - 10.11648/j.ijefm.20261403.14 T2 - International Journal of Economics, Finance and Management Sciences JF - International Journal of Economics, Finance and Management Sciences JO - International Journal of Economics, Finance and Management Sciences SP - 225 EP - 234 PB - Science Publishing Group SN - 2326-9561 UR - https://doi.org/10.11648/j.ijefm.20261403.14 AB - This study examines how FinTech platform service quality influences user loyalty in China, and focuses on two mediators: perceived switching costs and user trust. Data were collected from 290 Chinese commercial bank customers with active FinTech platform usage experience, using purposive sampling to ensure respondents had sufficient experience to evaluate the services. A hybrid Structural Equation Modeling-Artificial Neural Network (SEM-ANN) Approach is applied to test both linear and non-linear relationships. The findings from SEM show that service quality has positive effects on perceived switching costs, user trust, and user loyalty. User trust also positively affects loyalty. However, perceived switching costs do not show a significant direct effect on loyalty. This suggests that in mature markets, trust matters more than switching barriers. For mediation, user trust plays a significant partial mediating role. The indirect path through perceived switching costs is not significant. ANN sensitivity analysis confirms this: user trust has the highest predictive importance (100%), followed by service quality (78.29%). Perceived switching costs rank lowest (31.35%). This study makes contributions by verifying the dual-mediator model in China’s mature FinTech context, providing a framework for customer retention. Bank managers should build trust via service quality instead of artificial switching barriers. VL - 14 IS - 3 ER -

Yingyang School of Financial Technology, Zhejiang University of Finance and Economics, Hangzhou, China

School of Information Technology and Artificial Intelligence, Zhejiang University of Finance and Economics, Hangzhou, China

Information